If you want to avoid hefty deposits, unlock the best device financing deals and enjoy maximum flexibility with your cell phone plan, good credit is essential.

But what happens to your credit score during the plan application process or over the course of your contract?

Let’s break things down and see what’s really going on and how your cellphone plan might impact your credit score!

Be Careful When Hunting for Savings

If you’re not shopping around and comparing options, there’s a good chance that you’re overpaying for mobile phone service. Prices change regularly–as do plan allotments and features.

However, depending on how you shop around, you might find yourself causing more harm than good. Particularly if you’re applying for a monthly post-paid plan option or device financing.

When you apply for these types of services, most carriers run a credit check.

This is to see if you’re likely to pay your bill on time and ensure that you don’t have large amounts of debt already.

If you find that your first choice for service wants a large deposit, we recommend researching further options online instead of applying with another carrier.

This will reduce the number of hard checks on your credit report.

While the presence of these checks isn’t as bad as something like an account in collections or late payments, they can cost you a few points of that precious credit score you’ve worked so hard to build.

The amount of time these stay on your report varies. However, the inquiry may remain for up to 2 years in most areas.

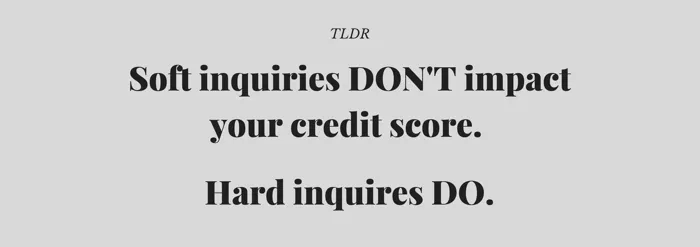

Hard Inquiries versus Soft Inquiries

How the check will impact your credit also depends on the type of check the carrier performs.

Inquiries come in two varieties: hard or soft.

In most cases, hard inquiries are used when a company is trying to make a lending decision–such as extending you a shiny new smartphone without an upfront deposit.

Soft inquiries are typically used for things like background checks, routine checks from banks, checking your own credit score or for pre-approved offers from businesses. They often happen without your explicit permission however they also don’t appear on your credit report or impact your credit score.

In most areas, running a hard inquiry requires your permission. This is because the inquiry will impact your credit score.

Credit Karma has a great guide on the finer differences between soft and hard credit checks to help assess the risks and outline examples of common inquiry scenarios.

If you’re curious what’s in your credit report, most credit bureaus offer at least one free report per year. Options include:

Paying My Cell Phone Bill On Time Helps My Credit, Right?

It seems reasonable that if contracts require a credit check, timely payments should help your credit score right?

This isn’t always true.

At the time of writing, prompt payment of your cellphone bill doesn’t show up on US credit reports.

If the carrier uses a third-party to offer device financing, that might show up–but that depends on the terms of the financing agreement.

However, regardless of where you live, late payments on your mobile bills or defaulting on your contract is sure to hit your credit score.

BONUS TIP

Though cellphone carriers in the US don’t report to credit bureaus, credit card companies do. Paying your cellphone bill with your credit card–and promptly paying off your credit balance–is a simple way to shift the reporting system in your favor!

Bad credit? Check with your local bank or credit union for a secured card. While most feature low credit limits, this minimizes the risk of debt running amok while still helping to rebuild your credit!

3 Ways to Reduce the Impact of Your Cellphone on Your Credit Score

There’s no reason that credit checks for cell phones should scare you. In most cases, if you pay your bill on time, there’s little reason for concern. These three tips can help:

Use an online tool to compare prices

If you’re looking for the best deals, you should start with Internet research. Our plan comparison tool outlines all the options from the best US carriers. This lets you sort through your options without sacrificing your credit score.

Go prepaid

As we mentioned in our recent guide–How to Get a Cell Phone Plan With Bad Credit–going with prepaid or no credit check plans removes the hassle–and potential damage–of a credit report entirely. If you don’t mind paying full price for a phone, features and service quality on prepaid plans rival those on monthly contracts

Sign up for Autopay

If you have no trouble paying bills financially but tend to lose track of due dates, autopay is a must-have. Some carriers will even shave a small amount off your monthly bill for using it! No late payments means no worries about future credit woes!

Your Turn

Credit is a complex topic. We hope this guide has helped answer any questions you might have.

If you found it useful, take a few seconds to share it with a friend!

If you have a question we didn’t cover, let us know in the comments below or send us a message. We monitor our comments closely and love hearing from the community!

Hi, I have a question about open a new account with Koodo. How many score do you expect to be lost during this process? And how soon do you expect it appears in your credit report? Thanks. I lost about 25 scores and it shows up in my credit repot after about one week. Is it normal situation?